Saudi Oil, OPEC's Ire

Saudi Oil, OPEC's Ire

Saudi King Abdullah wants to bring prices down to ensure long-term demand, but other OPEC ministers disagree

by Stanley Reed

BusinessWeek

It happens almost like clockwork. A few days before the end of every month, marketing executives from Saudi Aramco, Saudi Arabia's national oil company, ring up the likes of ExxonMobil (XOM) and Royal Dutch Shell (RDS), sounding them out about the oil they need and the price they would be willing to pay. The Saudis crunch the numbers, set a price, then call the global customers back to see how much they'd be willing to buy. By the 10th of the following month, customers—there are about 80 in all—are told how much crude they'll actually get.

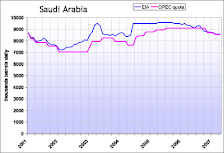

It's all part of an elaborate dance that goes on continually at OPEC's biggest producer. While the cartel may set production quotas for each member, the Saudis and a few other top suppliers frequently exceed those limits in order to meet world demand. And these days, the dance looks more like a tug-of-war, as the Saudis and their allies in the organization seek to contain crude prices while Iran and others want to keep them as high as possible. Saudi relations with OPEC "depend on where prices are; when prices are too high [the Saudis] side with consumers," says Vera de Ladoucette, senior director of consultancy Cambridge Energy Research Associates in Paris.

WARY OF HIGH PRICES

The tug-of-war is a key factor in the extraordinary volatility in prices lately. After soaring to $147 per barrel this summer, crude plummeted to below $90 in early September. On Sept. 22 it jumped again to $130 as traders scrambled to cover short positions and fretted about the U.S. economy, then fell to $107 as those pressures eased.

Why wouldn't the Kingdom want to squeeze the maximum out of customers? The Saudis have long memories and recall how high prices can cut into consumption; it happened in the 1980s and it's happening again now. Any threat to oil's leading role as a source of energy is a big worry for a country that sits on reserves of some 260 billion barrels. "We are concerned about the permanent destruction of demand," says a senior Saudi official. "Those who buy hybrid vehicles are not going back to SUVs."

OPEC hardliners such as Iran and Venezuela, by contrast, have less oil in the ground and are running short on cash, so they're more interested in maximizing revenues today. Friction within OPEC has been growing because Saudi Arabia has been pumping almost 10% more than its OPEC quota of 8.9 million barrels per day. The Saudis and other Persian Gulf states believe a price of $90 per barrel is about right, while the hardliners don't want to see anything less than $100 per barrel. "The current market is not balanced; it is oversupplied," Iranian OPEC representative Mohammad Ali Khatibi told Reuters.

Talk to the Saudis privately and they often express frustration with OPEC. Saudi negotiators complain that some members come to meetings with rigid political positions that don't take the real world into consideration. And the Saudis dismiss the likes of Venezuela and Iran for talking big without having the oil to back it up. Venezuela can't produce its quota of 2.5 million barrels per day, while Iran struggles to pump its 3.8 million. Only the Saudis have significant unused capacity that they can tap to influence the markets, and they are working to add to this margin.

The conflict flared this summer. Fearing that sky-high prices could blight oil's future, King Abdullah convened a conference of energy ministers and oil executives in the port city of Jeddah on June 22. At the meeting, the Saudis unilaterally announced a 200,000-barrel-a-day hike in production, on top of an increase of 300,000 barrels daily a few weeks earlier, annoying others in the producers' club. Algerian oil minister and current OPEC President Chekib Khelil called reporters to his hotel room to say he saw no need for the Saudi move.

It's clear the Saudis and Khelil don't see eye-to-eye. At a Sept. 9 OPEC conclave in Vienna, the Saudis went along with vague language promising a cut. But after the meeting they put out the word that they didn't feel bound by it. Khelil, meanwhile, held a 4 a.m. press conference at which he said the agreement required OPEC to cut output by 520,000 barrels per day—apparently violating an agreement with the Saudis, who would bear the brunt of any cut, not to mention a specific number.

The Saudis aren't about to abandon OPEC. But when it comes to pumping what the world needs to keep going, they will generally deliver what their customers want even if it goes against other members' wishes—which likely means more conflict in the producers' club. The Saudi production increases, says Christophe de Margerie, CEO of French oil giant Total (TOT), "are a coup de knife in the OPEC system."